Supply and Demand: an Introduction

A market for any good consists of all the buyers and sellers of that good. Due to scarcity, production and resources must be allocated

- Central planning: where all economic decisions are made centrally by a small group of individuals on behalf of a larger group.

- Free market: where production and distribution decisions are left to individuals interacting in private markets

Market concentration refers to the number and size of firms in a market, while market power is the ability of an individual firm to influence price by altering output. Any market can have:

- High concentration: small number of large firms, hence high market power

- Low concentration: large number of small firms, hence low market power

- Price takers: those who must accept the market price and have little control over price

- Price makers: those who can control price by restricting output due to little competition

Market Demand and Supply

We analyse market demand and supply under the assumption of ceteris paribus and that the market is in perfect competition, i.e. no participants has enough market power to set prices:

- Low market concentration

- No government intervention and regulations

- Everyone is a price taker

- No non-price related competition, e.g. advertising, brand names

- Homogeneous products, i.e. all products are identical

- Ease of entry/exit for new sellers

Demand Curve

The demand curve is a representation of the relationship between the amount of a particular good or service that buyers want to purchase in a given time period and the price of that good or service. If we add up all the individual demand curves, we have the demand curve of the market.

Changes in demand caused by a change in price occur for 2 reasons:

- Substitution effect: where other goods or services become more or less expensive relatively, i.e. people switch out to cheaper alternatives

- Income effect: where the purchasing power of a buyer’s income changes

Supply Curve

The supply curve is a representation of the relationship between the amount of a good or service that sellers want to supply in a given time period and the price of that good. Supply increases with price because suppliers can make a greater profit

Buyer’s reservation price: the most a buyer is willing to pay for a good or service.

Seller’s reservation price: the least amount for which a seller would be willing to sell an additional unit, usually equal to the marginal cost.

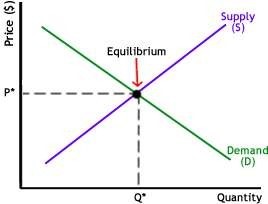

Market Equilibrium

In economics, equilibrium is where neither the price nor the quantity of a particular good or service is changing. The price and quantity to achieve this is known as the equilibrium price and equilibrium quantity. This point is given by the point of intersection between the demand and supply curve.

In market equilibrium, all buyers and sellers are satisfied with their respective quantities at the market price

Change in Equilibrium

- Excess Supply (Surplus): Prices above the equilibrium point leads to competition between sellers for less demand from buyers, eventually lowering price to equilibrium.

- Excess Demand (Shortage): prices below equilibrium leads to greater demand thus incentive for more suppliers, eventually raising price to equilibrium

In an unregulated market, any changes to equilibrium will eventually revert back to the equilibrium. However, in a regulated market, governments may introduce:

- Price ceiling: the maximum allowable price, specified by law

- Price floor: the minimum allowable price, specified by law

Shift in Demand Curve

- Proportional to price of the compliments. Two products are compliments in consumption if an increase in the price of one causes a fall in demand for the other

- Inversely proportional to price of substitutes. Two products are substitutes in consumption if an increase in the price of one causes a rise in demand of the other

- A normal good’s demand curve shifts right with increase in income, people want more of it

- An inferior good’s demand curve shifts left with increase in income, people want less of it

- Increase preference by buyers

- Increase in population of potential buyers

- An expectation of higher prices in the future, people buy more to stock up now

Shift in Supply Curve

- Decrease in costs of inputs

- Improvements in technology that reduces production costs

- Improvements in weather, for agricultural products

- Increase in number of suppliers

- Expectation of lower prices in the future

Economic Surplus

- Buyer’s surplus is the difference between the buyer’s reservation price and the price they actually pay

- Seller’s surplus is the difference between the price received by the seller and their reservation price

- Total economic surplus is the sum of the buyer’s surplus and the seller’s surplus

The Equilibrium Principle:

A market in equilibrium leaves no unexploited opportunities for individuals, i.e. no “cash on the table”, but may not exploit all gains achievable through collective group actions. A market out of equilibrium still offers surplus but some transaction won't take place so there is surplus, or cash on table, not exploited.

The socially optimal quantity of any good is the quantity that results in the maximum possible difference between the total benefits and total costs from producing the good. It takes into account of all costs, not just monetary costs. E.g. total cost of car production also takes into account the pollution it emits.

Therefore, socially optimal quantity is usually different to the actual equilibrium quantity, which only takes into account private costs. When a quantity of a good is:

- Less than the socially optimal quantity, boosting production increases the surplus of benefits over costs

- More than the socially optimal quantity, reducing its production increases total surplus

Economic efficiency occurs when all goods and service in the economy are produced and consumed at their respective socially optimal quantities. It reflects how efficiently resources are being used. A market is ONLY efficient if it is in equilibrium i.e. no cash on table.

The Efficiency Principle:

Efficiency is an important social goal, because when the economic pie grows larger, it is possible for everyone to have a larger slice